Single Currency Derivatives#

Single currency derivatives are examples of the simplest two-leg structures.

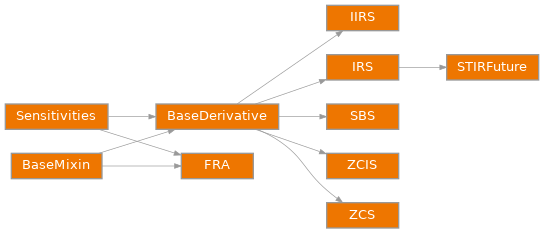

Abstract base class with common parameters for many |

|

|

Create an interest rate swap composing a |

|

Create a single currency basis swap composing two |

|

Create a forward rate agreement composing single period |

|

Create a zero coupon swap (ZCS) composing a |

|

Create a zero coupon index swap (ZCIS) composing an |

|

Create an indexed interest rate swap (IIRS) composing an |

|

Create a short term interest rate (STIR) future. |