Replicating a SOFR Curve & Swap from Bloomberg’s SWPM#

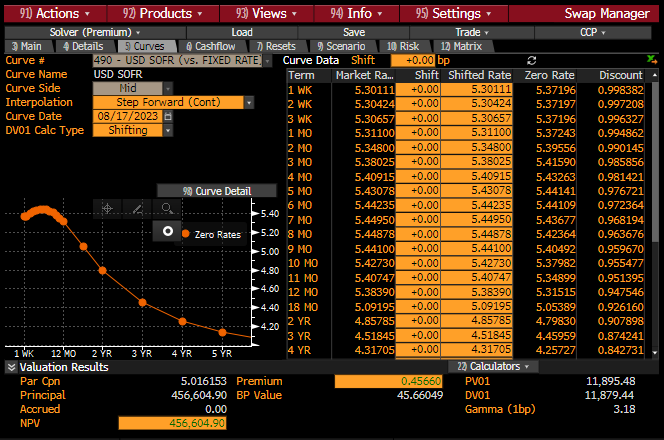

At a point in time on Thu 17th Aug 2023 loading the SWPM function in Bloomberg presented the following default SOFR curve data:

We can replicate the input data for the Curve in a table as follows:

In [1]: data = DataFrame({

...: "Term": ["1W", "2W", "3W", "1M", "2M", "3M", "4M", "5M", "6M", "7M", "8M", "9M", "10M", "11M", "12M", "18M", "2Y", "3Y", "4Y"],

...: "Rate": [5.30111, 5.30424, 5.30657, 5.31100, 5.34800, 5.38025, 5.40915, 5.43078, 5.44235, 5.44950, 5.44878, 5.44100, 5.42730, 5.40747, 5.3839, 5.09195, 4.85785, 4.51845, 4.31705],

...: })

...:

In [2]: data["Termination"] = [add_tenor(dt(2023, 8, 21), _, "F", "nyc") for _ in data["Term"]]

In [3]: with option_context("display.float_format", lambda x: '%.6f' % x):

...: print(data)

...:

Term Rate Termination

0 1W 5.301110 2023-08-28

1 2W 5.304240 2023-09-05

2 3W 5.306570 2023-09-11

3 1M 5.311000 2023-09-21

4 2M 5.348000 2023-10-23

5 3M 5.380250 2023-11-21

6 4M 5.409150 2023-12-21

7 5M 5.430780 2024-01-22

8 6M 5.442350 2024-02-21

9 7M 5.449500 2024-03-21

10 8M 5.448780 2024-04-22

11 9M 5.441000 2024-05-21

12 10M 5.427300 2024-06-21

13 11M 5.407470 2024-07-22

14 12M 5.383900 2024-08-21

15 18M 5.091950 2025-02-21

16 2Y 4.857850 2025-08-21

17 3Y 4.518450 2026-08-21

18 4Y 4.317050 2027-08-23

Bloomberg defaults to a “Step Forward (cont)” interpolation mode, this is effectively the

same as “log_linear” in rateslib’s formulation for Curves. We will configure DF

nodes dates to be on the termination date of the swaps:

In [4]: sofr = Curve(

...: id="sofr",

...: convention="Act360",

...: calendar="nyc",

...: modifier="MF",

...: interpolation="log_linear",

...: nodes={

...: **{dt(2023, 8, 17): 1.0}, # <- this is today's DF,

...: **{_: 1.0 for _ in data["Termination"]},

...: }

...: )

...:

Now we will calibrate the curve to the given swap market prices, using a global

Solver, passing in the calibrating instruments and rates.

In [5]: sofr_args = dict(effective=dt(2023, 8, 21), spec="usd_irs", curves="sofr")

In [6]: solver = Solver(

...: curves=[sofr],

...: instruments=[IRS(termination=_, **sofr_args) for _ in data["Termination"]],

...: s=data["Rate"],

...: instrument_labels=data["Term"],

...: id="us_rates",

...: )

...:

SUCCESS: `func_tol` reached after 5 iterations (levenberg_marquardt), `f_val`: 3.116743265440467e-17, `time`: 0.0562s

In [7]: data["DF"] = [float(sofr[_]) for _ in data["Termination"]]

In [8]: with option_context("display.float_format", lambda x: '%.6f' % x):

...: print(data)

...:

Term Rate Termination DF

0 1W 5.301110 2023-08-28 0.998382

1 2W 5.304240 2023-09-05 0.997208

2 3W 5.306570 2023-09-11 0.996327

3 1M 5.311000 2023-09-21 0.994862

4 2M 5.348000 2023-10-23 0.990145

5 3M 5.380250 2023-11-21 0.985856

6 4M 5.409150 2023-12-21 0.981421

7 5M 5.430780 2024-01-22 0.976721

8 6M 5.442350 2024-02-21 0.972364

9 7M 5.449500 2024-03-21 0.968194

10 8M 5.448780 2024-04-22 0.963676

11 9M 5.441000 2024-05-21 0.959670

12 10M 5.427300 2024-06-21 0.955477

13 11M 5.407470 2024-07-22 0.951395

14 12M 5.383900 2024-08-21 0.947546

15 18M 5.091950 2025-02-21 0.926160

16 2Y 4.857850 2025-08-21 0.907898

17 3Y 4.518450 2026-08-21 0.874241

18 4Y 4.317050 2027-08-23 0.842731

Notice that the DFs are the same as those in SWPM (at least to a visible 1e-6 tolerance).

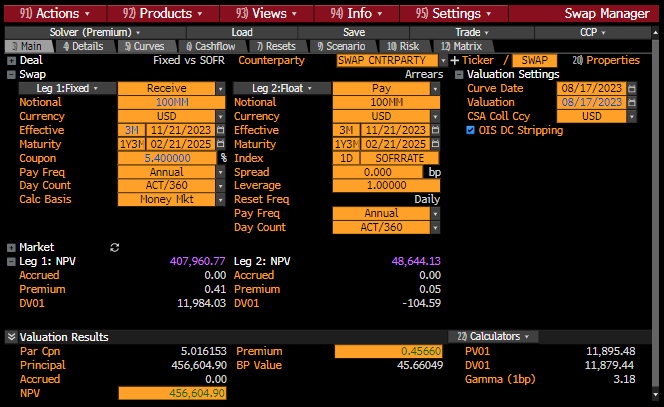

Next we will create a swap in SWPM and also create the same swap in rateslib. The metrics that SWPM and rateslib generate for npv, delta (DV01), gamma and analytic delta (PV01) are the same to within a very small tolerance.

In [9]: irs = IRS(

...: effective=dt(2023, 11, 21),

...: termination=dt(2025, 2, 21),

...: notional=-100e6,

...: fixed_rate=5.40,

...: curves="sofr",

...: spec="usd_irs",

...: )

...:

In [10]: irs.npv(solver=solver)

Out[10]: <Dual: 456622.098604, (sofr0, sofr1, sofr2, ...), [0.0, 0.0, 0.0, ...]>

In [11]: irs.delta(solver=solver).sum()

Out[11]:

local_ccy display_ccy

usd usd -11879.94

dtype: float64

In [12]: irs.gamma(solver=solver).sum().sum()

Out[12]: 3.176665278863451

In [13]: irs.analytic_delta(curve=sofr)

Out[13]: <Dual: -11896.008577, (sofr0, sofr1, sofr2, ...), [-0.0, -0.0, -0.0, ...]>

Finally we can double check the cashflows and cashflows_table of the swap.

In [14]: irs.cashflows_table(solver=solver)

Out[14]:

local_ccy USD

collateral_ccy NaN

payment

2024-02-23 -7613.74

2025-02-25 501239.07

In [15]: irs.cashflows(solver=solver)

Out[15]:

Type Period Ccy Acc Start Acc End Payment Convention DCF Notional DF Collateral Rate Spread Cashflow NPV FX Rate NPV Ccy

leg1 0 FixedPeriod Stub USD 2023-11-21 2024-02-21 2024-02-23 act360 0.26 -100000000.00 0.97 None 5.40 NaN 1380000.00 1341464.35 1.00 1341464.35

1 FixedPeriod Regular USD 2024-02-21 2025-02-21 2025-02-25 act360 1.02 -100000000.00 0.93 None 5.40 NaN 5490000.00 5082380.28 1.00 5082380.28

leg2 0 FloatPeriod Stub USD 2023-11-21 2024-02-21 2024-02-23 act360 0.26 100000000.00 0.97 None 5.43 0.00 -1387613.74 -1348865.48 1.00 -1348865.48

1 FloatPeriod Regular USD 2024-02-21 2025-02-21 2025-02-25 act360 1.02 100000000.00 0.93 None 4.91 0.00 -4988760.93 -4618357.05 1.00 -4618357.05